Many people believe that the rich once paid much more in taxes as a percentage of their income since top marginal rates were once much higher. The reality, however, is that a combination of relatively higher brackets, larger deductions, and tax avoidance and the like actually reduced the effective rates to MUCH less than is popularly believed.

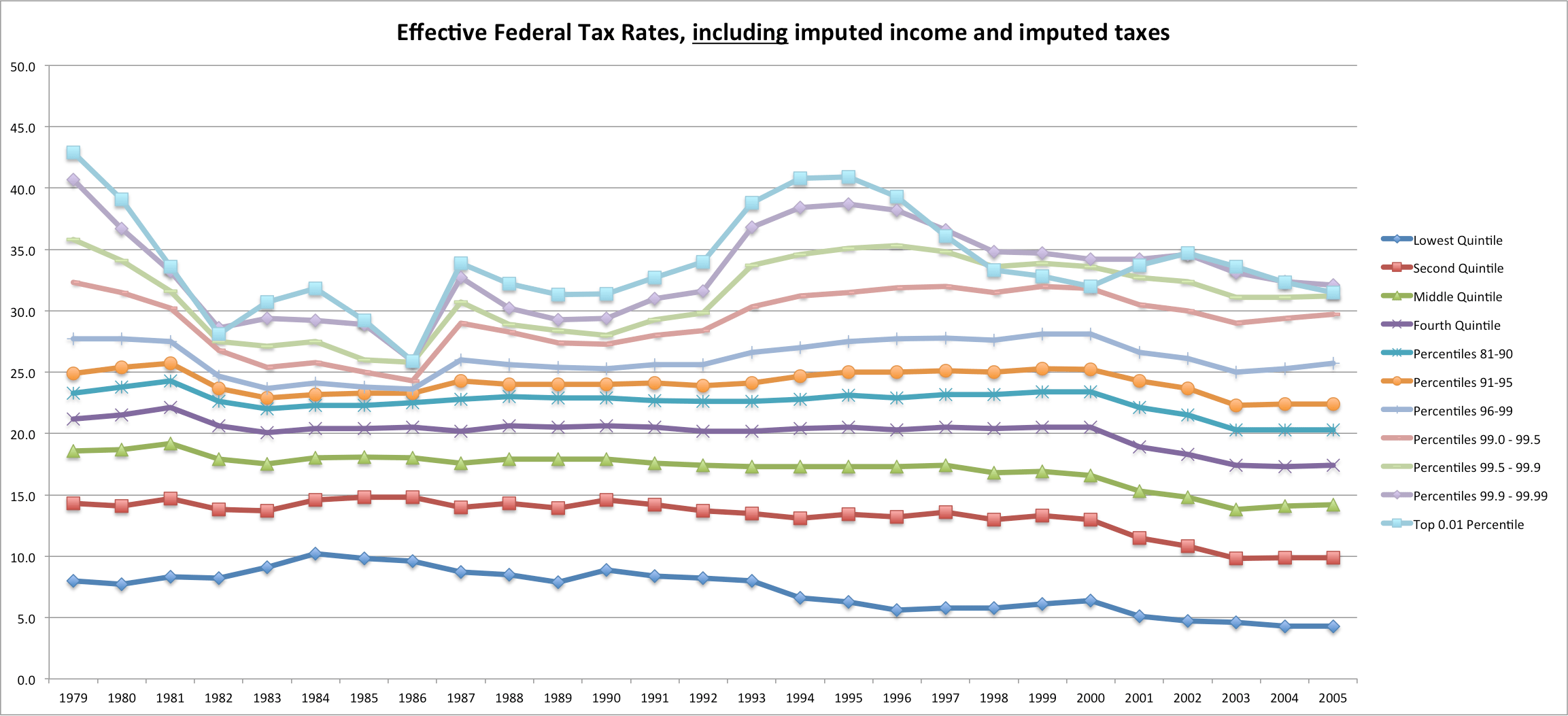

The CBO published some data a few years ago to break down effective tax rates amongst higher income groups (they usually aggregate the top 1% as one big group), so here is a chart to actually reveal the truth.

According to their calculations,the rich did pay a bit more in 1979 (the late 70s probably had abnormally high ETRs due to bracket creep and the like). That said, they also imputed 100% corporate income taxes to shareholders (mostly the rich) and the employer-portion of payroll taxes to both the numerator and the denominator [in other words, they assume that the tax payer would have had correspondingly more income and thus add both the the numerator and the denominator of this calculation]

Since many of these same progressives have trouble with this concept (e.g., they wish to assert that Romney only paid a ~15% ETR) I thought it’d be helpful to illustrate what this would look like if we subtracted both of these imputed income sources/tax burdens. This, in other words, would more closely resemble one’s ETR if they divided the total federal taxes paid by their AGI [although this also includes the miniscule burden added by federal excise taxes]